If you’re still chasing approvals in email, rebuilding reports in Excel, and asking three different teams for the same numbers at month-end, your finance function isn’t short on effort. It’s short on architecture.

That’s the position many mid-market Australian and New Zealand businesses are in right now. The team works hard, but the core finance process is fragmented. Payroll sits in one system. Inventory lives somewhere else. Procurement relies on workarounds. Consolidation happens late. By the time the board pack is ready, part of it is already out of date.

Digital transformation in finance matters because that operating model stops scaling long before the business does. Growth exposes every weak join. New entities create more intercompany complexity. Regulatory obligations around GST, Super, AASB reporting, payroll, and data handling don’t wait for the ERP project to catch up.

The answer isn’t buying more software and hoping integration sorts itself out later. It’s building a finance operating model where systems, controls, and reporting work together by design. That’s where an architecture-led approach changes the conversation from “which tool should we buy?” to “how should finance run?”

The End of the Month-End Scramble

Most finance leaders know the pattern. The month closes, then the core work starts. Reconciliations are still manual. Spreadsheet versions multiply. One entity has posted late journals. Another has coded expenses differently. Someone in operations has a number that doesn’t match finance, and now the CFO is stuck deciding which version goes into the report.

That isn’t a technology problem alone. It’s a structural problem. Finance has usually grown around legacy systems, local fixes, and urgent business decisions. Over time, those decisions create process debt. The team compensates with extra effort, but extra effort isn’t the same as control.

A modern finance function runs differently. Transaction processing is automated where it should be. Master data is governed properly. Approvals follow policy. Reporting draws from a unified source, not from stitched-together extracts. The close becomes a controlled process rather than a monthly recovery exercise.

Finance teams don’t need more dashboards built on unstable data. They need fewer handoffs, cleaner process ownership, and systems that reflect how the business actually operates.

That’s the practical lens to bring to digital transformation in finance. It’s not an IT vanity project, and it isn’t code for replacing good people with software. It’s the work of removing avoidable friction so finance can spend less time assembling facts and more time advising the business.

For AU/NZ organisations, that shift is especially important in businesses carrying legacy ERP constraints, multiple entities, inventory complexity, or regulated reporting obligations. The opportunity is real, but only if the operating model is designed with local compliance and day-to-day execution in mind.

What Digital Transformation Really Means for Finance

Digital transformation in finance gets reduced to buzzwords far too often. In practice, it means replacing disconnected finance work with an operating model that is automated, connected, and visible in near real time. A useful analogy is the shift from driving with a paper map to driving with live GPS. The destination may be the same, but the way you find your way changes completely.

Finance teams that want a grounded explanation often benefit from understanding digital transformation within the finance department, especially when the goal is to connect technology choices to operating outcomes instead of abstract innovation language.

Intelligent automation

Automation is the first pillar, but not in the shallow sense of digitising paper forms. Good finance automation removes repetitive effort from reconciliations, approvals, invoice capture, expense processing, journal workflows, and exception routing.

That’s where tools around the ERP matter. A business might use Lightyear or Zudello for invoice capture, Medius for AP workflow, ProSpend or Webexpenses for spend governance, and BlackLine for reconciliation discipline. The ERP remains the core record, but automation handles the operational grind around it.

The practical outcome is straightforward:

- Fewer manual touchpoints, which reduces rekeying and approval bottlenecks

- Clearer control points, because workflows are defined in the system rather than in email chains

- More analyst time for judgement, not just transaction processing

Unified data

The second pillar is unified data. On this front, many projects succeed or fail.

Finance can’t produce reliable insight when entities, products, warehouses, employees, and customers are defined differently across systems. If payroll, CRM, procurement, warehouse, and ERP platforms all use different structures, the reporting layer becomes a translation exercise. Teams then spend month-end trying to reconcile definitions instead of interpreting performance.

A stronger model connects the ecosystem properly. Workato, Celigo, Boomi, and Jitterbit are common options for integrating ERP with payroll, WMS, CRM, HR, banking, and eCommerce. KeyPay and ELMO may feed workforce data. HubSpot or Salesforce may feed customer and pipeline context. CartonCloud or 3DLogistiX may carry warehouse events that finance needs for landed cost, fulfilment, or margin analysis.

Practical rule: if a KPI depends on manual export, cleanup, and re-upload, it isn’t yet part of a transformed finance process.

That’s also why the breakthrough in AI isn’t just model access. It’s context, structure, and meaning. The article on why interpretation matters more than AI novelty captures this well for finance leaders dealing with messy operational data.

Real-time reporting

The third pillar is real-time reporting, or at least reporting that is materially closer to live operations than a static month-end pack. This doesn’t mean every business needs a control tower on day one. It means the CFO should be able to see cash, liabilities, inventory exposure, margin movement, and entity performance without waiting for spreadsheet consolidation to finish.

Here’s the fundamental shift. Finance stops acting as historian and starts acting as adviser.

That changes roles, not just tools. Controllers spend less time policing data assembly and more time reviewing exceptions. Finance managers spend less time preparing the same report every month and more time challenging assumptions. CFOs get time back for capital allocation, pricing, covenant visibility, and strategic planning.

What it does not mean

Digital transformation in finance does not mean ripping out every system immediately. It does not mean adding AI to broken processes. It does not mean selecting software before defining process ownership, data design, and control requirements.

In solid programmes, people stay central. The strongest teams redesign workflows with the users who perform them. They test reporting definitions early. They define approval authority clearly. They train to real scenarios, not generic software demos.

That’s what makes transformation stick.

Key Drivers and Measurable Benefits for AU/NZ Businesses

A CFO in Brisbane or Auckland usually does not start a finance transformation because technology feels dated. The trigger is operational strain. The board wants faster reporting. Auditors want cleaner evidence. The business adds entities, warehouses, subscription revenue, or cross-border complexity, and finance is still relying on reconciliations that live in spreadsheets and inboxes.

Why urgency is higher in AU and NZ

Mid-market businesses across Australia and New Zealand face a specific mix of pressure. Growth often comes before finance architecture is ready for it. A manufacturer rolling out another warehouse needs tighter inventory valuation and cleaner landed cost treatment. A services group expanding into New Zealand needs entity-level visibility, intercompany discipline, and reporting that can stand up to scrutiny. A wholesale distributor facing margin pressure needs procurement, stock, and finance data to line up fast enough to support pricing and purchasing decisions.

Local compliance raises the stakes. GST treatment, Super obligations, payroll handoffs, and AASB reporting requirements do not get simpler because the business is growing. They get harder to manage if core systems were never designed to work together.

That is why architecture matters. NetSuite, Epicor Kinetic, and MYOB Acumatica can all support a stronger finance model in the right context, but only if the data structure, approval design, integration pattern, and reporting logic are set up properly from the start.

What measurable improvement actually looks like

The benefit case is usually easier to defend than finance leaders expect. I rarely see a mid-market program approved because of one headline metric alone. It gets approved because several operating improvements land at once.

Month-end closes shorten because reconciliations and approvals sit inside the system instead of across email chains. Audit preparation gets easier because the transaction trail is visible without manual evidence gathering. Cash visibility improves because AP, AR, purchasing, and bank data stop living in separate places. Finance teams spend more time reviewing exceptions and less time assembling reports.

The trade-off is straightforward. Standardising processes inside the ERP often means giving up a few local workarounds that teams have become attached to. In practice, that is usually a good exchange if it removes duplicate data entry, weak approval control, and reporting delays.

For many CFOs, the first strategic decision is infrastructure. This guide to cloud vs on-premise ERP for finance leaders is useful when the business case depends on control, upgrade path, integration needs, and internal IT capacity.

A well-structured program tends to produce four board-level outcomes:

- Faster reporting cycles, because entity consolidation, allocations, and approvals are handled with less manual intervention

- Stronger control execution, because workflows, segregation of duties, and audit trails are built into day-to-day transactions

- Better cash and margin visibility, because finance can see committed spend, receivables exposure, inventory position, and profitability with less lag

- Lower scaling friction, because adding a new entity, site, or product line does not require another layer of spreadsheets to keep reporting together

Benefits that hold up in the real world

The strongest results come from fixing structural problems, not from adding features for their own sake.

A cloud ERP with well-designed integrations can support multi-entity reporting, auditability, approval discipline, and inventory-finance alignment far better than a disconnected legacy stack. The surrounding ecosystem matters too. Coupa can improve procurement governance. Kyriba can strengthen treasury visibility. Zone and Co can extend NetSuite finance operations. Avalara can help where tax automation is part of the requirements. AI also has a role, but only when the underlying data model is stable and the use case is clear. Most finance teams are better served by a staged plan such as this enterprise generative AI strategy roadmap than by rushing into generic AI pilots.

One test I use is simple. If the board asks for a different cut of revenue, margin, or working capital, can finance produce it quickly and defend the numbers?

If the answer is yes, the architecture is doing its job. If the answer still depends on spreadsheet rewrites, offline adjustments, and screenshots for approvals, the finance function has not modernised yet, even if new software is already live.

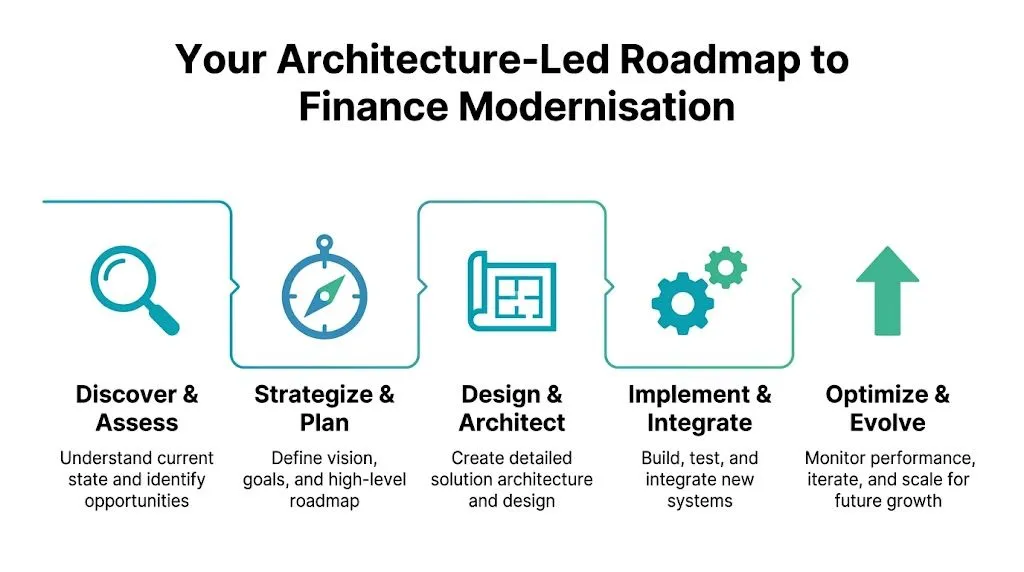

Your Architecture-Led Roadmap to Finance Modernisation

Finance modernisation succeeds or fails long before the build starts. The decisive work is architectural. If the operating model, controls, data ownership, and integration approach are vague, the project usually turns into an expensive software deployment that leaves finance still fixing numbers in spreadsheets at month-end.

Discover and assess

Start with how finance runs today across the business, not with a vendor comparison. Review close activities, AP, AR, procurement, payroll handoff, inventory valuation, project costing, consolidations, and management reporting at process level. In Australian and New Zealand mid-market firms, the weak points are often found in handoffs between systems, entities, and outsourced providers rather than inside a single finance process.

The assessment should identify four things:

- Process friction, where approvals, reconciliations, and manual work slow the team down

- Data inconsistency, where customer, supplier, item, or chart data differs across systems

- Control gaps, where audit evidence relies on emails, screenshots, or tribal knowledge

- Architecture risk, where legacy applications limit integration, reporting, or scale

This work usually changes the investment decision. Some businesses need a full ERP replacement. Others can get a better result by standardising processes, retiring one or two problem systems, and fixing integration design before replacing the core platform.

Strategise and plan

The next step is to define the target operating model in business terms a CFO can defend. Faster close, cleaner board reporting, tighter cash control, better project margin visibility, fewer audit adjustments, stronger procurement discipline. Those outcomes need to be agreed before platform selection gets too far ahead.

For AU/NZ businesses, local requirements need to be designed in early. That includes GST treatment, Super obligations, payroll interfaces, AASB reporting needs, intercompany treatment, and the practicalities of operating across multiple entities or jurisdictions. If those requirements are left until build, teams usually end up adding exceptions that weaken controls and increase support costs.

A sound planning document should answer a short list of practical questions:

- Which processes need one standard way of working across entities or business units

- Which reports need to be reliable from day one for board, lender, audit, and management use

- Which local compliance requirements need system support from the start, including GST, Super, payroll, and statutory reporting

- Which integrations are required for go-live, and which can wait until phase two

AI should be treated the same way. Start with clear use cases, data readiness, and governance. The enterprise generative AI strategy roadmap is useful because it frames adoption as a staged capability decision, not a rushed add-on to an ERP project.

Design and architect

This stage decides whether the future state will hold up under growth, acquisitions, audit scrutiny, and operating change.

Platform choice needs to follow business fit. Oracle NetSuite often works well for multi-entity groups that need strong financial management, consolidation, and a broad add-on ecosystem. Epicor Kinetic is often the better fit where manufacturing, scheduling, MES, and cost visibility matter. MYOB Acumatica can be a strong option for growing AU/NZ businesses that want flexible cloud ERP across finance and operations without overcomplicating the stack.

The architecture should then define the parts that usually cause rework later:

- Integration patterns, using tools such as Workato, Celigo, Boomi, or Jitterbit

- Data ownership, especially for customers, suppliers, items, employees, and chart segments

- Security and access design, based on role, segregation of duties, and audit requirements

- Reporting architecture, so KPI definitions stay consistent across entities and systems

- Extension strategy, for AP automation, treasury, spend control, WMS, payroll, or HR

At this point in the journey, businesses often bring in implementation partners such as OneKloudX to run architecture-led discovery, compare NetSuite, Epicor Kinetic, and MYOB Acumatica properly, and shape an integration approach that fits Australian and New Zealand operating conditions.

For finance leaders still weighing hosting and control trade-offs before finalising the architecture, this guide on cloud versus on-premise ERP for financial leaders is a useful reference.

The ERP should support the next stage of the business. If the design cannot absorb a new entity, changed approval flows, or another specialist system, finance will rebuild workarounds within a year.

Implement and integrate

Good implementation programs are phased, but they are not slow. The aim is to reduce risk while protecting reporting integrity and business continuity.

A practical sequence usually starts with the finance foundation: general ledger, AP, AR, banking, approval workflows, master data, and core reporting. After that, the business can add procurement, expense management, payroll integration, warehouse connectivity, planning, or treasury based on value and dependency. This order matters because every downstream tool depends on clean structures upstream.

Testing needs to reflect real operating conditions. Use actual GST scenarios, intercompany journals, approval paths, payroll handoff cases, inventory adjustments, and reconciliations. Generic scripts often show that the software works. They do not show that the business can close accurately under pressure.

Optimise and evolve

Go-live is the start of finance governance in the new environment. Without ongoing ownership, approval rules drift, reports multiply, integration errors sit unresolved, and local compliance changes get patched in too late.

Post-implementation review should cover process exceptions, role access, report usage, reconciliation effort, integration failures, and changes in business structure. That is particularly important for mid-market firms adding new entities, warehouses, product lines, or offshore operations.

The strongest finance environments are managed as an evolving capability. Architecture, controls, and reporting standards are reviewed regularly, so the system keeps supporting growth instead of sending the team back to spreadsheets.

Digital Finance Transformation in Action Across Industries

At 4:30 pm on the second business day of the month, three finance teams can be facing three very different problems. A manufacturer is arguing over standard versus actual costs. A distributor is chasing stock variances across warehouses. A services group is trying to reconcile intercompany charges between Australia and New Zealand before the board pack goes out. All three are doing finance transformation. None should be using the same design.

Manufacturing in Western Sydney

A mid-market manufacturer usually raises a finance issue that sounds straightforward. Margins by job are inconsistent. Inventory write-offs keep appearing. Finance spends month-end reconciling what the shop floor believes happened against what landed in the ERP.

In practice, that points to an architecture problem, not just a reporting problem. Production, inventory, labour capture, and costing are often running on different assumptions. Epicor Kinetic is a strong fit where the business needs tighter control across BOMs, WIP, scheduling, procurement, and financial posting. Add MES capability and disciplined master data, and finance can see variance drivers earlier, before they become quarter-end surprises.

The primary gain is confidence in operational numbers. That matters when a CFO is setting pricing, reviewing plant performance, or deciding whether a product line still earns its place.

Distribution across multiple locations

Distributors tend to have a different failure point. The issue is usually stock visibility by site, replenishment quality, purchasing discipline, and whether warehouse activity is reflected cleanly in finance.

A national distributor running Oracle NetSuite might connect Netstock for demand planning, CartonCloud or 3DLogistiX for warehouse execution, and SPS Commerce for retailer connectivity. Done well, that gives finance a cleaner view of landed cost, committed spend, fulfilment timing, margin by branch, and aged inventory risk.

The trade-off is complexity. Every extra platform can improve a specific process, but each integration adds another point where controls can drift if ownership is unclear. That becomes more important in Australia when procurement and supplier reporting need to support broader governance obligations, including Modern Slavery reporting in some organisations.

Strong results depend as much on operating discipline as software selection. Teams that want better adoption usually need a clear change plan across warehouse leads, procurement, customer service, and finance. This guide on managing internal change for a successful ERP implementation is relevant here because distribution projects often fail in the handoff between system design and day-to-day behaviour.

Multi-entity services across Australia and New Zealand

Services groups usually struggle somewhere else. The pressure sits in multi-entity reporting, project billing, payroll integration, intercompany allocations, and management reporting that has to work across both sides of the Tasman.

MYOB Acumatica can suit this model well, particularly for mid-market firms that want stronger group visibility without rebuilding every report in spreadsheets. When it is integrated properly with payroll and HR platforms such as KeyPay or ELMO, and with AP and expense tools such as Expensify, Webexpenses, or Lightyear, finance can reduce manual rework and tighten control over approvals, coding, and cross-entity reporting.

For AU and NZ businesses, local requirements shape the design. GST treatment, Super obligations, AASB reporting expectations, and NZ entity structures all affect how chart of accounts, tax logic, approval workflows, and entity-level reporting should be configured. Generic global templates often miss that.

Good transformation work standardises controls where it should, then reflects how the business actually earns revenue, incurs cost, and meets local compliance obligations.

Where AI fits in

AI has a role in each of these settings, but only after the transaction flow is clean. Tools such as Cauzzy AI can help with anomaly detection, forecasting support, and exception monitoring. They are useful when master data, posting rules, and process ownership are already under control.

Used on poor finance data, AI produces faster noise. Used on well-structured ERP data, it helps finance leaders spot issues earlier and make better operating decisions.

Navigating Common Transformation Hurdles in Australia

A typical Australian month-end failure does not start at month-end. It starts months earlier, when finance accepts another manual workaround between the ERP, payroll, banking, and reporting stack. By the time the CFO sees delayed consolidations, GST review issues, or unexplained balance sheet movements, the root cause is usually already embedded in the architecture.

In the mid-market, the recurring problems are familiar. Legacy integrations break under volume. Data ownership sits in too many hands. Local compliance is treated as a testing item instead of a design input. Scope expands faster than decision-making can keep up.

Legacy integration usually fails at the handoff points

Many AU and NZ businesses have grown by acquisition, added systems in stages, or customised around an older ERP because it was faster at the time. The result is a finance environment made up of an ERP, payroll platform, WMS, CRM, banking feeds, and spreadsheet-based reconciliations that nobody wants to touch before go-live.

That architecture creates risk in ordinary places. Tax codes fail to map cleanly between systems. Customer and supplier records drift. Intercompany postings need manual correction. A payment file works in test but fails under real approval conditions.

The right response is architectural triage. Assess which integrations support control, reporting, and compliance. Replace brittle file transfers where they create finance risk. Leave lower-value edge cases for a later phase if they do not affect close, cash, tax, or audit outcomes.

For businesses considering NetSuite, Epicor Kinetic, or MYOB Acumatica, this matters early. Each platform can support a solid finance model, but only if the surrounding integration decisions are made with the target operating model in mind, not just the shortest implementation path.

Compliance has to shape the design from day one

Australian and New Zealand finance teams do not get much room for generic global templates. GST logic, Super obligations, AASB reporting, payroll controls, approval authority, and document retention all affect how the system should be configured.

I have seen projects pass functional testing and still create finance pain because the chart of accounts was too loose, audit trail requirements were not thought through, or entity structures did not reflect how the group reports. Those are not minor clean-up items. They affect close speed, external review, and confidence in the numbers.

Treat compliance as a design requirement. That means finance, implementation partner, payroll stakeholders, and in some cases external advisors need to make decisions early on tax treatment, posting rules, role permissions, approval paths, and record retention.

Resistance usually points to a design flaw

Finance teams rarely resist change for its own sake. They push back when the future process is unclear, when approval controls look weaker, or when the new workflow adds time under month-end pressure.

That concern is often valid.

The AP lead who questions a new intake process may be spotting an exception path that has not been handled. The financial controller who challenges a reporting workflow may be protecting an audit requirement the project team has missed. Good programs use that feedback before build decisions harden.

Three practices help:

- Define role changes early, especially for approvals, reconciliations, master data ownership, and reporting sign-off

- Train against real finance scenarios, including month-end, disputed invoices, payroll exceptions, and intercompany issues

- Give line managers a practical change plan, not just slide decks and broad project updates

If adoption risk is building, this guide to managing internal change for a successful ERP implementation is a useful reference.

Data discipline belongs with finance, not only IT

Poor master data turns a good system into a slow close. Duplicate vendors, weak account structures, inconsistent item naming, and conflicting customer hierarchies all flow into reporting, reconciliations, and audit preparation.

Finance should own the records that drive financial truth. IT can support controls and integration. The business still needs clear accountability for chart design, tax logic, approval metadata, entity mapping, and reporting definitions.

This work is rarely popular, but it pays back quickly. A clean data model improves transaction accuracy, reduces rework, and gives CFOs more confidence in board reporting and forecast conversations.

Scope drift usually starts with reasonable requests

Transformation programs in Australia often get overloaded because every workstream has a defensible ask. Operations wants one more workflow. Sales wants CRM changes included. HR wants payroll redesign brought forward. Finance wants reporting finished in full before phase one closes.

Without tight sequencing, the project slows, costs rise, and core finance outcomes get diluted.

A better pattern is to protect the first operating model. Lock the processes needed for close, payables, receivables, cash, tax, and statutory reporting. Phase the rest based on business value and dependency. That takes active sponsorship from the CFO, not just project coordination.

Mid-market businesses in AU and NZ usually get better ROI when they modernise in controlled stages. The architecture stays cleaner, compliance risk stays lower, and the finance team gets usable improvements sooner.

Building Your Future-Proof Finance Ecosystem

The core ERP matters, but it won’t carry the whole finance function on its own. Long-term value comes from the ecosystem around it, the integration layer, the approval workflows, the AP tools, the payroll connection, the treasury visibility, the warehouse touchpoints, and the governance that keeps all of it aligned.

The partner decision is strategic

Choosing an implementation partner is not the same as choosing software. Finance leaders need a team that understands local compliance, operating realities in manufacturing and distribution, and the difference between a clean architecture decision and a shortcut that becomes expensive later.

A useful partner selection lens includes:

- Architecture capability, not just configuration capability

- AU/NZ operating knowledge, especially around GST, Super, payroll, and local reporting practices

- Integration fluency, across middleware, WMS, payroll, CRM, procurement, and banking

- Post-go-live support, because optimisation and health checks protect the original investment

- Commercial honesty, including willingness to phase work instead of overloading scope

The businesses that get the most from digital transformation in finance usually treat the partner relationship as ongoing operational capability, not as a one-off deployment event.

The ecosystem is where finance becomes scalable

The difference between “ERP installed” and “finance modernised” becomes obvious.

A scalable finance ecosystem may include:

- Spend and procurement controls, with ProSpend, Coupa, Medius, or Webexpenses

- Invoice capture and AP automation, through Lightyear or Zudello

- Payroll and people data integration, with KeyPay or ELMO

- Treasury and cash visibility, through Kyriba

- Close and reconciliation discipline, with BlackLine

- Integration orchestration, via Workato, Celigo, Boomi, or Jitterbit

- Warehouse and logistics connections, through CartonCloud, 3DLogistiX, or SPS Commerce

- CRM and revenue alignment, with HubSpot or Salesforce

- Governance and controls support, through tools such as Salto or Strongpoint where change management and system controls matter

Not every organisation needs every tool. The point is to assemble the right operating stack for the business model, then govern it properly.

The finance function you’re building

The end state isn’t “more digital”. It’s more dependable.

Finance should be able to close without heroics, explain margin without detective work, support growth without rebuilding its reporting logic, and respond to audit or board questions without chasing evidence across inboxes. That requires disciplined design, the right platform choice, and an ecosystem that fits the business.

The KPI discussion also needs to stay grounded. Track outcomes that finance leaders can use.

| Category | KPI | Example Target Improvement |

|---|---|---|

| Close process | Month-end close cycle | Move from prolonged manual close to a materially shorter, controlled close |

| Reporting | Management reporting timeliness | Deliver reports earlier with fewer manual adjustments |

| AP operations | Invoice approval cycle | Reduce approval delays through workflow automation |

| Cash visibility | Daily cash position clarity | Improve visibility through connected banking and payable data |

| Inventory finance | Stock and margin accuracy | Improve confidence in valuation and margin reporting |

| Compliance | Audit trail completeness | Strengthen traceability across approvals and transactions |

| Integration | Manual data handoffs | Reduce spreadsheet-based transfers between systems |

| Adoption | User process compliance | Increase use of standard workflows over side processes |

The finance leaders who get this right don’t treat transformation as a project with a finish date. They treat it as the operating foundation for the next stage of growth.

If your finance team is still carrying too much process debt, OneKloudX can help you assess the current state, shape an architecture-led roadmap, and align Oracle NetSuite, Epicor Kinetic, or MYOB Acumatica with the controls, integrations, and reporting your AU/NZ business needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}